Stationarity in time series

A stationary time series has constant mean, constant variance, and autocorrelations that depend only on the lag, not on time. Most time series models assume stationarity. Detecting and correcting non-stationarity is the essential first step before fitting AR, MA, ARIMA, or any other model.

Formal definition

A time series \(\{y_t\}\) is weakly stationary (or covariance-stationary) if:

\[E[y_t] = \mu \quad \forall t \qquad \text{(constant mean)}\] \[\text{Var}(y_t) = \sigma^2 < \infty \quad \forall t \qquad \text{(constant variance)}\] \[\text{Cov}(y_t, y_{t+k}) = \gamma(k) \quad \forall t \qquad \text{(autocovariance depends only on lag } k \text{)}\]

Strict stationarity requires the entire joint distribution of \((y_t, y_{t+1}, \ldots, y_{t+k})\) to be invariant to time shifts. For practical purposes, weak stationarity is sufficient.

A series that is not stationary is called non-stationary or integrated. The most common form of non-stationarity in economic and financial data is the unit root: a stochastic trend that causes the series to wander without mean-reverting.

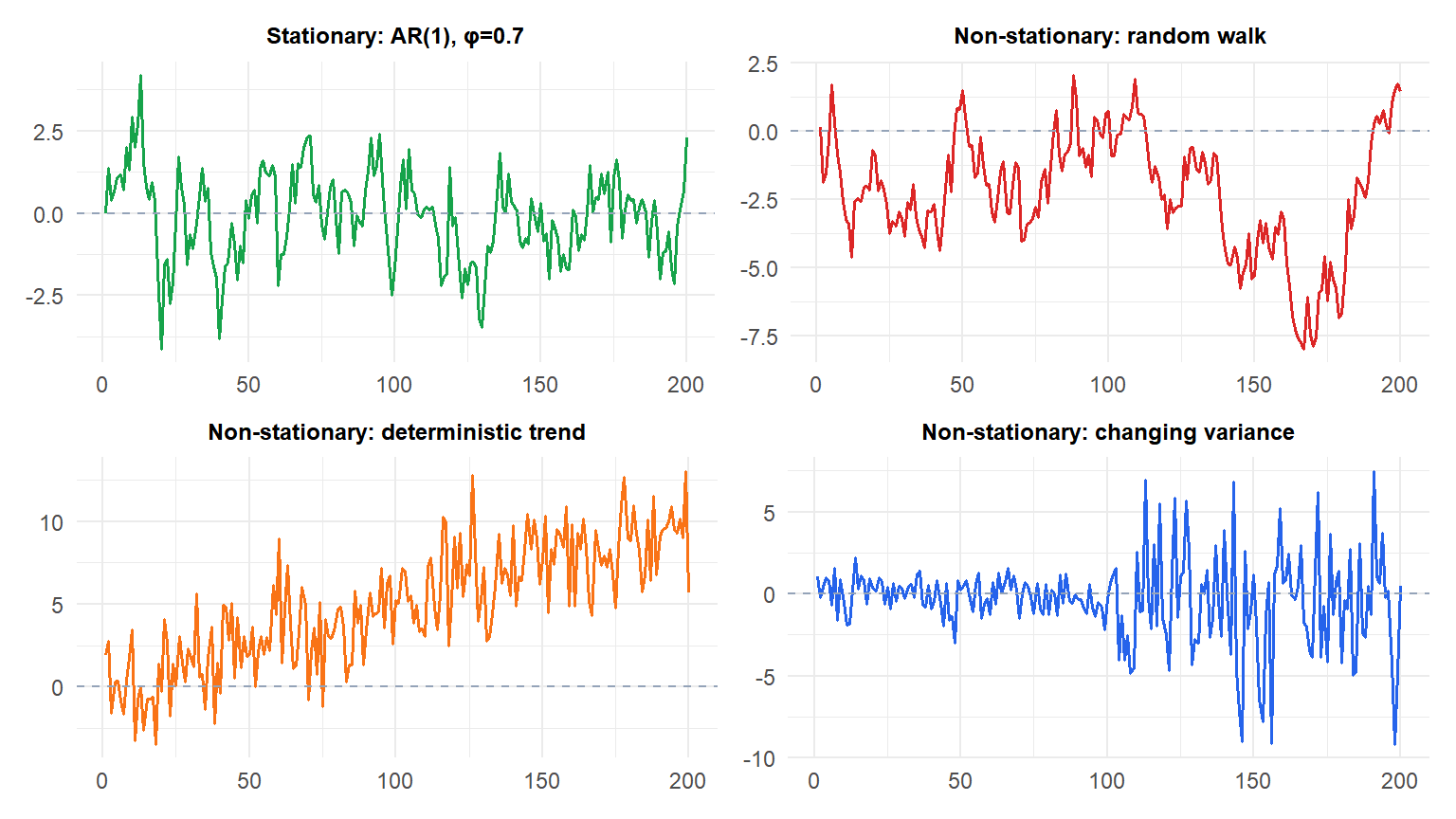

The stationary series (green) fluctuates around a constant mean. The random walk (red) drifts without bound. The trended series (orange) has a rising mean. The heteroscedastic series (blue) has variance that changes mid-sample.

Unit roots and random walks

The most important source of non-stationarity in practice is the unit root. An AR(1) process:

\[y_t = \phi y_{t-1} + \varepsilon_t\]

is stationary when \(|\phi| < 1\) (the series reverts to its mean). When \(\phi = 1\), it becomes a random walk:

\[y_t = y_{t-1} + \varepsilon_t \implies y_t = y_0 + \sum_{s=1}^t \varepsilon_s\]

The variance of a random walk grows without bound: \(\text{Var}(y_t) = t\sigma^2\). Shocks are permanent: they never dissipate. This is why testing for \(\phi = 1\) (a unit root) is central to time series analysis.

Testing for stationarity

Augmented Dickey-Fuller (ADF) test

Tests \(H_0\): the series has a unit root (non-stationary) vs \(H_1\): the series is stationary. The test fits the regression:

\[\Delta y_t = \alpha + \beta t + \gamma y_{t-1} + \sum_{j=1}^p \delta_j \Delta y_{t-j} + \varepsilon_t\]

and tests \(H_0: \gamma = 0\) (unit root present). Reject \(H_0\) if the t-statistic for \(\gamma\) is sufficiently negative (critical values are non-standard, not from the normal distribution).

The number of lags \(p\) is chosen to remove autocorrelation from the residuals (typically by AIC or BIC).

KPSS test (Kwiatkowski-Phillips-Schmidt-Shin)

Tests the opposite: \(H_0\): the series is stationary vs \(H_1\): the series has a unit root. Large values of the KPSS statistic reject stationarity.

⚠️ ADF and KPSS have opposite null hypotheses - do not confuse them

The most common mistake: treating both tests as if they test the same thing.

- ADF: \(H_0\) = unit root (non-stationary). A large p-value means you fail to reject non-stationarity. A small p-value means you reject the unit root, supporting stationarity.

- KPSS: \(H_0\) = stationarity. A large p-value means you fail to reject stationarity. A small p-value means you reject stationarity.

Interpreting: “ADF p-value = 0.60, therefore the series is stationary” is wrong. A p-value of 0.60 means you failed to reject the unit root, i.e., you have no evidence against non-stationarity.

Use both tests together. If ADF rejects the unit root AND KPSS does not reject stationarity: strong evidence for stationarity. If both fail to agree: investigate further.

Phillips-Perron (PP) test

A nonparametric alternative to ADF. Same \(H_0\) (unit root), but uses a different correction for autocorrelation in the residuals instead of adding lagged differences. Tends to be more robust to heteroscedasticity.

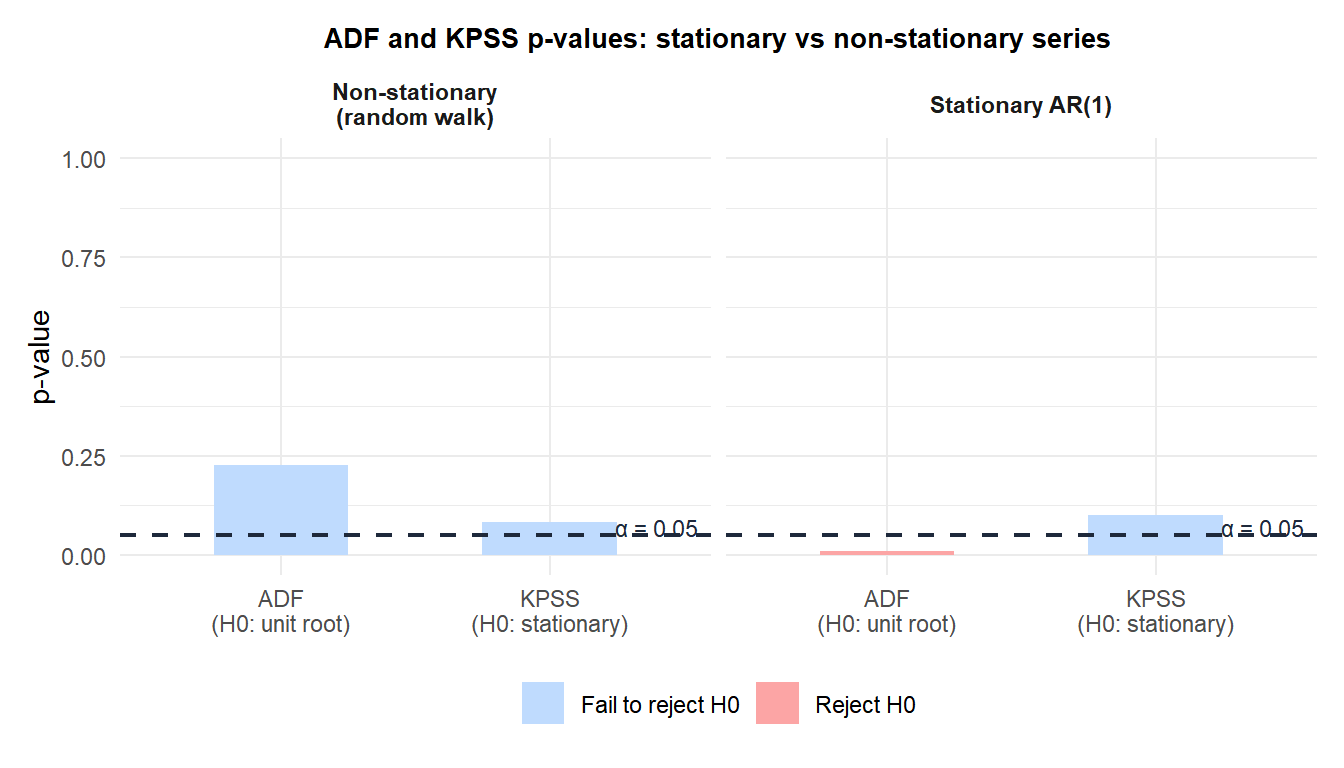

For the stationary AR(1): ADF rejects the unit root (red, \(p < 0.05\)) and KPSS fails to reject stationarity (blue, \(p > 0.05\)). Both agree: stationary. For the random walk: ADF fails to reject the unit root (blue) and KPSS rejects stationarity (red). Both agree: non-stationary.

Transformations to achieve stationarity

Differencing

The standard remedy for a unit root. First difference removes a linear stochastic trend:

\[\Delta y_t = y_t - y_{t-1}\]

A series that becomes stationary after \(d\) differences is called integrated of order \(d\), denoted \(I(d)\). Most economic series are \(I(1)\): one difference suffices.

Log transformation

Stabilizes variance that grows proportionally with the level (common in prices, GDP, sales). \(\log(y_t)\) converts multiplicative seasonality to additive and makes the series more symmetric.

Box-Cox transformation

A family of power transformations parameterized by \(\lambda\):

\[y_t^{(\lambda)} = \begin{cases} (y_t^\lambda - 1)/\lambda & \lambda \neq 0 \\ \log(y_t) & \lambda = 0 \end{cases}\]

The optimal \(\lambda\) is estimated from the data. \(\lambda = 1\) is no transformation; \(\lambda = 0\) is log; \(\lambda = 0.5\) is square root.

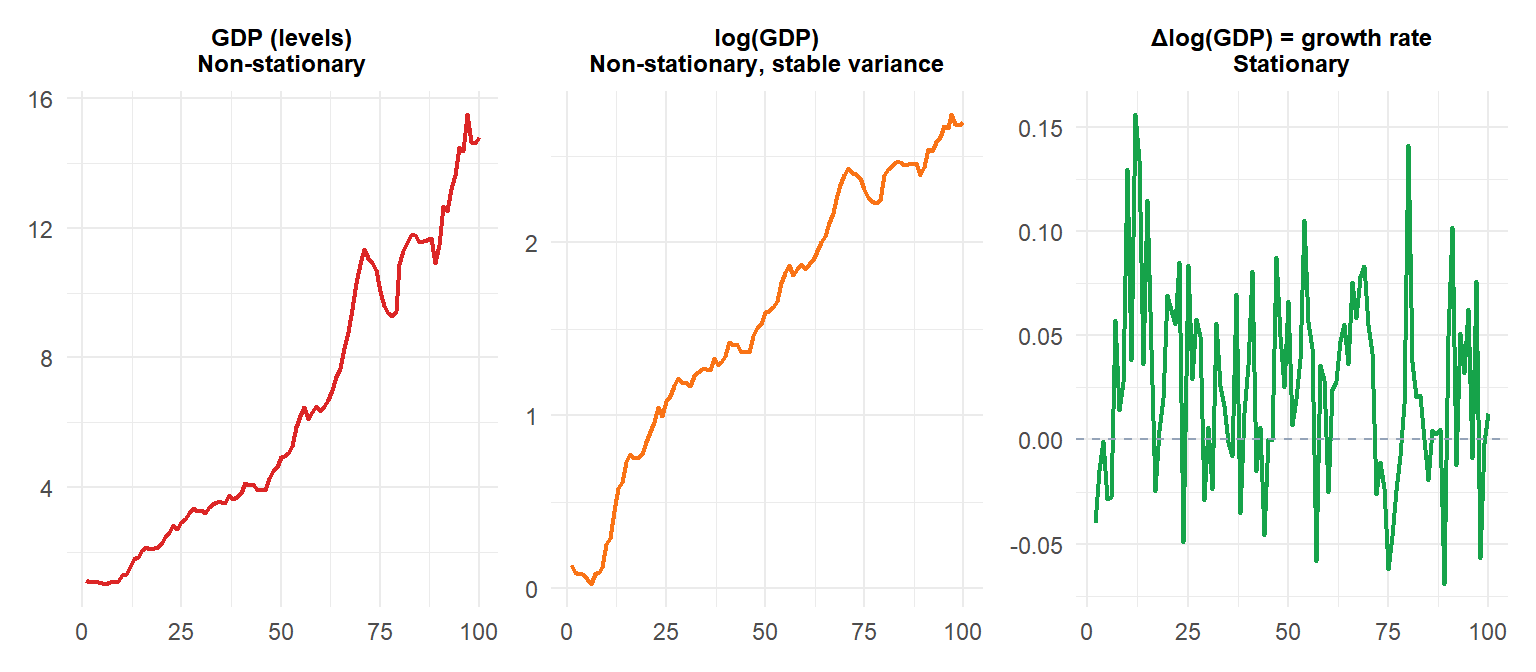

GDP in levels (red) is non-stationary with growing variance. After log (orange), variance stabilizes but the trend remains. After first-differencing log(GDP) (green), the series becomes stationary: it represents the GDP growth rate, fluctuating around a constant mean.

How many differences?

Apply the ADF test after each differencing step until stationarity is achieved. For most economic series, \(d=1\) suffices. Over-differencing (applying more differences than needed) makes the series harder to model and should be avoided.

A practical rule: if the ADF test on the original series fails to reject the unit root, difference once and test again. If the ADF on \(\Delta y_t\) rejects the unit root, \(d=1\) is appropriate.

💡 Stationarity tests in R

library(tseries)

# ADF test (H0: unit root)

adf.test(y)

adf.test(diff(y)) # after first differencing

# KPSS test (H0: stationary)

kpss.test(y)

# Phillips-Perron test (H0: unit root)

pp.test(y)

# Automatic differencing order selection

library(forecast)

ndiffs(y) # number of regular differences needed

nsdiffs(y) # number of seasonal differences needed